Data centers on the rise?

The rise of data centers around the world has come about as a result of the shift toward the digital economy. More and more data need to be stored in secured locations and accessed at the quickest possible time.

As a result, data center REITs have been on the rise with many companies investing more in their data solutions. In Singapore, there are 3 such REIT companies involved heavily in the investment and management of data centers and here we go:

Data Centre REIT #1 - Keppel DC REIT

Keppel DC REIT (KREIT) is the first data center real estate investment trust listed in Asia and primarily invests in real estate assets for data centres and also digital economy purposes.

KREIT has assets spread out across the world in countries such as Singapore, Australia, China, Malaysia, Germany, Ireland, Italy, the Netherlands, and the United Kingdom.

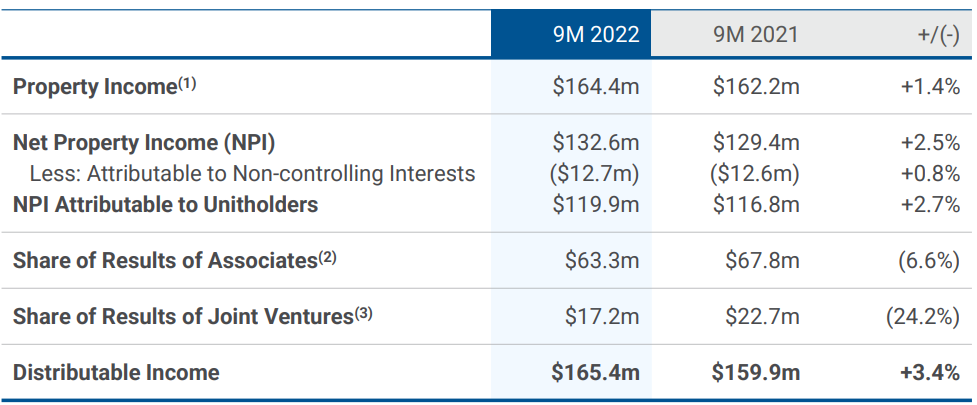

For the 9 months of 2022, the distributable income of KREIT grew by 3.4% to SGD165.4 million compared to SGD159.9 million in the first 9 months of 2021. This was due mainly to the acquisition of Keppel Bay Tower and adjustments of income tax from the previous years.

Currently, KREIT has about SGD9.0 billion of assets under management (AUM), with Singapore having the highest percentage of AUM at 78.6% followed by Australia (18.2%) and South Korea (3.2%).

Keppel DC REIT could be a worthy investment opportunity for the following reasons:

- High and improving occupancy rates from 95.5% in 2Q 2022 to 96.8% in 3Q 2022.

- Low cost of debt at 2.1%.

- Distribution of an additional SGD100 million over 5 years in tandem with the 20th anniversary in 2026.

KREIT has a call of OVERWEIGHT from most analysts, with an average target price of SGD1.00. This implies an upside of 17.0% from the share price of SGD0.855.

Meanwhile, KREIT trades at a low price-to-book ratio of 0.65x, lower than the industry average of 0.87x, and produces an enticing dividend yield of 6.9%.

Data Centre REIT #2 - Mapletree Industrial Trust

Mapletree Industrial Trust is a real estate investment trust investing in income-producing real estate assets that consists mainly of industrial and data centers. More specifically, MaIT's portfolio assets consist of data centers, business park buildings, flatted factories, slack-up/ramp-up buildings, and light industrial buildings.

It has about 85 and 56 assets in Singapore and United States respectively. Out of these assets, about 54.6% of them consist of data centers, followed by high-tech buildings (16.4%) and flatted factories (16.4%).

For the 1st half of 2022, Mapletree Industrial Trust's revenue grew by 21.0% to SGD343.3 million compared to SGD283.6 million in the first half of 2021. However, due to higher property operating, borrowing and trust expenses, the distributable income only grew by 5.9%.

Mapletree Industrial Trust currently has about SGD8.9 billion of assets under management, where it has quadrupled in size since 2010.

Mapletree Industrial Trust could be worth taking a good look at for the following factors:

- Reputable tenants such as HP, AT&T, and Bank of America.

- High total occupancy rate of 95.6%.

- Strong backing from Mapletree Investments, who manage SGD78.7 billion of assets in the world.

Hence, most analysts have Mapletree Industrial Trust at an OVERWEIGHT call with an average target price of SGD2.52. This means an implied upside of 12% from the current share price of SGD2.26.

In terms of valuation, Mapletree Industrial Trust is trading at a price-to-book ratio of 1.28x and sports a dividend yield of around 6% - although the DPU has came down slightly in FY2023 onwards.

Data Centre REIT #3 - Digital Core REIT

Digital Core REIT (DCREIT)'s principal activity is to invest in assets centered around data centers and the digital economy. It currently manages about USD1.45 billion of assets in the United States and Canada mainly.

Most of its data centers are located in Northern Viriginia at USD629 million, followed by Silicon Valley (USD479 million) and Toronto (USD203 million).

Revenue of DigiCore REIT came in 1.6% higher at USD80.7 million compared to the forecast of USD79.4 million. However, due to distribution adjustments, distributable income is actually 3.4% lower compared to the forecast.

DigiCore REIT could be a good investment to hold for the following reasons:

- High exposure to the U.S. market with established tech companies having high demand for data center services.

- 100% occupancy rate since IPO in December 2021.

- Expansion plans into Frankfurt, Germany and Dallas, U.S.

As a result, most analysts have DigiCore REIT with a BUY call and an average target price of SGD0.72. This implies an upside of 35.8% compared to the current share price of SGD0.53.

As DigiCore REIT has been embroiled in the situation where some of its tenants have gone bankrupt due to the poor macroeconomic situation in US, its P/B has declined to around 0.64x, the lowest among the 3 digital centre reits mentioned here.

Build your Dividend Growth Portfolio

When REIT expert Augustine has a stock tip, it can pay to listen. After all, he has already semi-retired with the passive income generated from his portfolio of REITs and Dividend stocks.

Augustine just revealed what he believes could be the ‘5 best REITs’ for investors to buy right now… And together with his co-expert James, they will manage a $200K Model Portfolio with up to 20 REITs + Dividend Growth Stocks!

Thus, if you want a fuss-free way to build your dividend growth portfolio… and also to mingle with like-minded income investors…

Wait no longer and click on the button to join our membership here:

https://www.patreon.com/Invest_Kaki!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}