The REIT sector has seen a slight rebound from its lows recently due to a slight decline in the 10 year treasury yield as well as Trump wants a lower rates environment.

Investors who love REITs can turn to Retail REITs as this REIT segment is more resilient in nature compared to office and industrial REITs. In this article, I shall write about 3 Singapore retail REITs with yields of 5% or higher.

Frasers Centrepoint Trust

Frasers Centrepoint Trust is one of the largest suburban retail mall owners in Singapore.

Its Singapore retail portfolio include Causeway Point, Century Square, Hougang Mall, NEX (effective 50.0%-interest), Northpoint City North Wing (including Yishun 10 Retail Podium), Tampines 1, Tiong Bahru Plaza, Waterway Point (effective 50.0%-interest) and White Sands.

For the full year ended 30 September 2024, FCT reported revenue was down 4.9% to S$351.7 million while net property income decreased by 4.6% to S$253.3 million. This is mainly due to the divestment of Changi City Point and on-going AEI at Tampines 1

Despite the drop in property income, DPU remained stable with only a slight dip of 0.9% to 12.04 cents. This translate to a current dividend yield of 5.4% based on the current price of S$2.22.

Portfolio occupancy remained very healthy at 99.7%. Tenants’ sales increased by 1.2%. Rental reversion was a positive 7.7%. Gearing ratio remained below 40% at 38.5%. Average cost of debt is 4.1% with interest coverage ratio of 3.41 times.

With dividend yield of 5.4% and given its resilient nature of owning suburban malls, FCT is one of the 3 Singapore retail REITs with yields of 5% or higher. You can view the REIT website here.

CapitaLand Integrated Commercial Trust

CICT is one of the largest Singapore commercial real estate owner. CICT’s portfolio comprises 21 properties in Singapore, two properties in Frankfurt, Germany, and three properties in Sydney, Australia with a total property value of S$26.0 billion.

In Singapore, it owns retail malls such as Bedok Mall, Bugis+, Bugis Junction, Tampines Mall, Westgate, IMM building etc.

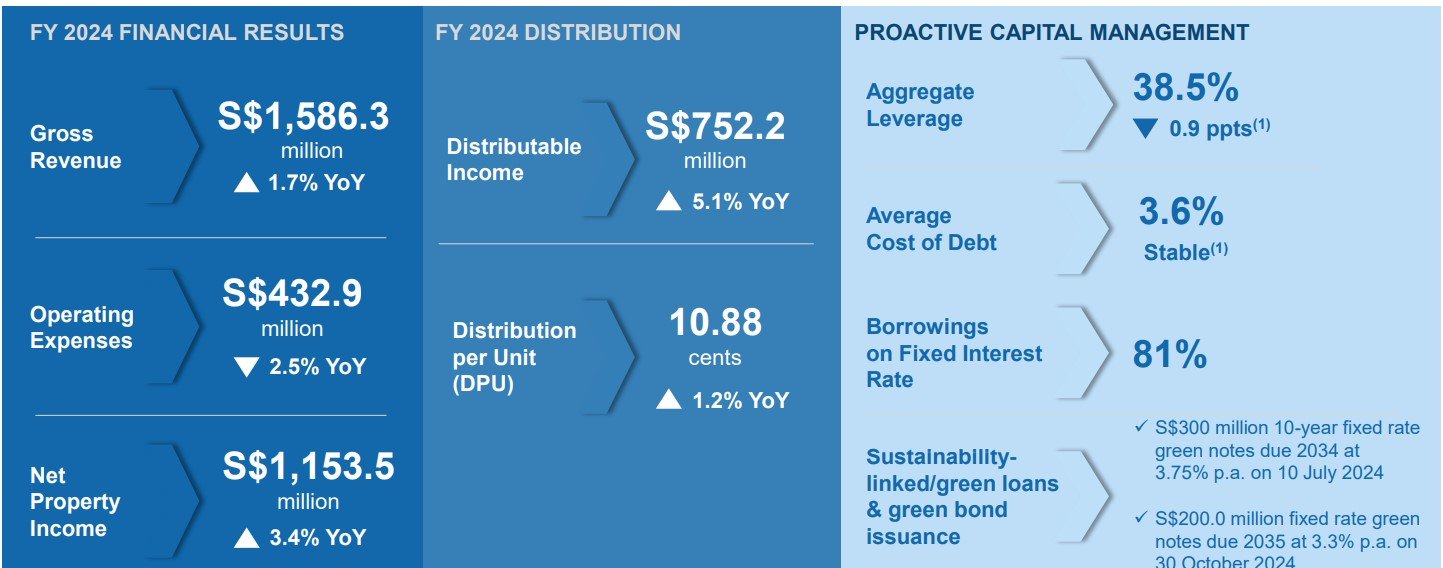

For the full year ended 31 Dec 2024, CICT reported gross revenue up 1.7% to S$1.58 billion while net property was up 3.4% to S$1.15 billion. DPU increased by 1.2% to 10.88 cents which translate to a dividend yield of 5.1%.

Portfolio occupancy remains healthy at 96.7%. Gearing ratio was below 40% at 38.5% with average cost of debt of 3.6%. Interest coverage ratio was at 3.1 times. 81% of borrowings were on fixed rates.

Given the high occupancy of its retail malls at 99.3% and with a dividend yield of 5.1%, CICT is one of the 3 Singapore retail REITs with yields of 5% or higher. You can view the REIT website here.

Starhill Global REIT

Starhill Global REIT owns retail malls in Singapore, Australia, Malaysia, Japan and China, valued at about S$2,762 million(1) as at 30 June 2024. In Singapore, Starhill Global owns Wisma Atria and Ngee Ann City.

For the first half ended 31 Dec 2024, Starhill Global reported revenue was up by 1.7% to S$96.3 million while net property income increased by 1.6% to S$75.6 million. First half DPU inched up 1.1% to 1.8 cents. This translate to an annualized dividend yield of 7.2%.

Portfolio occupancy was 97.7%. Gearing ratio was below 40% at 36.2%. Interest cover was at 2.9 times with average interest cost of 3.69%. 83% of the debts were on fixed rates.

With a high dividend yield of 7.2%, Starhill Global is definitely one of the 3 Singapore retail REITs with yields of 5% or higher. You can view the REIT website here.

Disclaimer: Please note that the REITs mentioned in this article are not a financial recommendation to buy and investors need to do their own research and due diligence before investing in any of these REITs.