Amid the market sell-off in the past few weeks, the STI index has shed 556.33 points or 15.4% from the peak of 3615.28 in May 2018 to a low of 3058.95 last Friday.

With such weakness in the stock market, you might be wondering whether it is the time now to enter the market. To be honest, we do not know when is the right time to go in the market. In fact, no one can forecast the future too.

That said, what we can do is to check out companies worth putting on our watchlist right now.

In this article, we will show you 3 cheap stocks with attractive dividend yields.

#1 Ban Leong Technologies Limited (SGX: B26)

Ban Leong Technologies is mainly involved in technology distributing business. Some of the multimedia products distributed by them are such as earphones, speakers, cameras and commercial and consumer displays. The company has been distributing technology products for 25 years. Since then, it has expanded its brand to 4 countries, including China, Thailand, Malaysia and Vietnam.

Other than IT distribution, Ban Leong also involves in logistics, tech support and product marketing business.

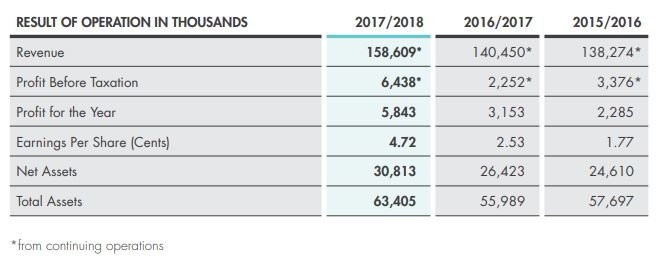

Financial performance for Ban Leong was improving at a modest rate. Revenue was growing at CAGR of 7.1% from S$138.3 million in FY15/16 to S$158.7 million in FY17/18. In addition, its earnings per share (EPS) was increasing at a whopping rate of 63%, from 1.77 cents in FY15/16 per share to 4.72 cents per share in FY17/18.

Source: Ban Leong Technologies Limited Annual Report 2017/2018

According to their annual report, there has been a small percentage of growth in sales on the online platform. Although the sales were relatively small, the management expects that the figures to improve as the younger generation are preferring online purchases.

Besides, the company is exploring opportunities in China and Hong Kong by working with like-minded parties to expand their presence in these markets. The management stated that they aim to penetrate their business into these market in the next two years.

As of October 19, 2018, Ban Leong Technologies Limited is trading at S$0.25 per share. This translates to a juicy dividend yield of 7% and a PE of merely 5.29x.

#2 Excelpoint Technology Limited (SGX: BDF)

Excelpoint Technology Ltd is an electronics components distributor providing components, engineering design services and supply chain management to original equipment manufacturers (OEM), original design manufacturers (ODM) and electronics manufacturing services (EMS).

It has a business presence in more than 40 cities across the Asia Pacific with a workforce of over 650 people from different nationalities and cultural backgrounds.

From the chart below, we can observe that the company’s total revenue was growing from USD$ 729 million in 2013 to USD$ 1.1 billion in 2017. EPS was hovering around USD$ 6.87 per share.

For FY2017, the company has paid out an ordinary dividend of S$0.03 per share and a special dividend of S$0.015 cents per share.

Source: Excelpoint Technology Limited Annual Report 2017

Looking forward, the company plans to tap into the growth in IoT segment.

The management mentioned that they have invested in the building of an IoT demonstration facility with cutting-edge technologies from their suppliers. This platform allows their customers to have access to applications that showcase those technologies.

On October 19, 2018, Excelpoint Technology Limited was trading at S$0.6 per share. It has a dividend yield of 5% and PE of 5.73.

#3 Tat Seng Packaging Group Limited (SGX: T12)

Tat Seng Packaging is involved in supplying corrugated packaging products. It designs and manufactures paper packaging products to pack a diverse range of goods according to customers’ specifications. The company operates in Singapore as well as the China market.

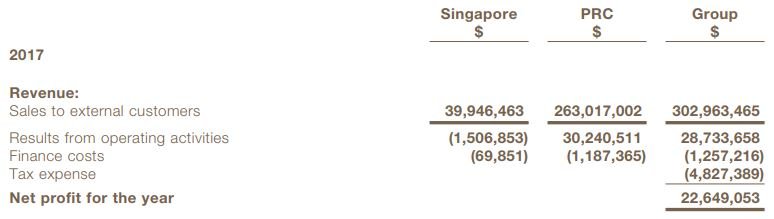

Most of the company’s revenue was generated from China, which accounts for 86.8% of the company’s total revenue. In FY2017, the amount of revenue generated in China was $263 million while Singapore segment contributed $39.9 million to the total revenue.

Source: Tat Seng Packaging Annual Report 2017

Despite having a relatively low valuation, Tat Seng Packaging’s financial performance was rather impressive.

It has recorded a topline growth from S$215.6 million in FY2013 to S$303 million in FY2017, which is equivalent to a CAGR of 8.88%. Its earning per share was growing at a rate of 14.49% in the past 4 years, from S$0.0753 in FY13 to S$0.1294 in FY17.

Besides that, the company has been paying a consistent dividend to its shareholders for the past five years. In FY2017, the company has paid out a total dividend of S$0.03 per ordinary share.

According to the annual report, the management is seeing a rising demand for corrugated products in the near future. This, in turn, would lead to an opportunity for growth for the company. The company plans to improve its operational efficiency in terms of cost management to boost productivity.

In addition, the company plans to invest and upgrade their machinery to reduce the reliance on labour, develop more relevant staff skills, build new capabilities through technological innovation and IT capabilities enhancement.

Tat Seng Packaging was closing at S$0.65 per share last Friday, with a dividend yield of 4.62% and PE of 4.46.

FREE Download - "7 Top Stocks Flashing On Our Watchlist"

Psst... We’ve found 7 exciting companies that are poised to skyrocket >100% in the years to come.

Simply click here to uncover these ideas in our FREE Special Report!

{kind=link}

{kind=link}

{kind=link}

{kind=link}